Pricing Convertible Bonds with the Penalty TF Model Using Finite Element Method

Published in Computational Economics, 2025

Recommended citation: Kazbek, R., Erlangga, Y., Amanbek, Y., & Wei, D. (2025). Pricing convertible bonds with the penalty TF model using finite element method. Computational Economics, 1-28. https://doi.org/10.1007/s10614-024-10625-1

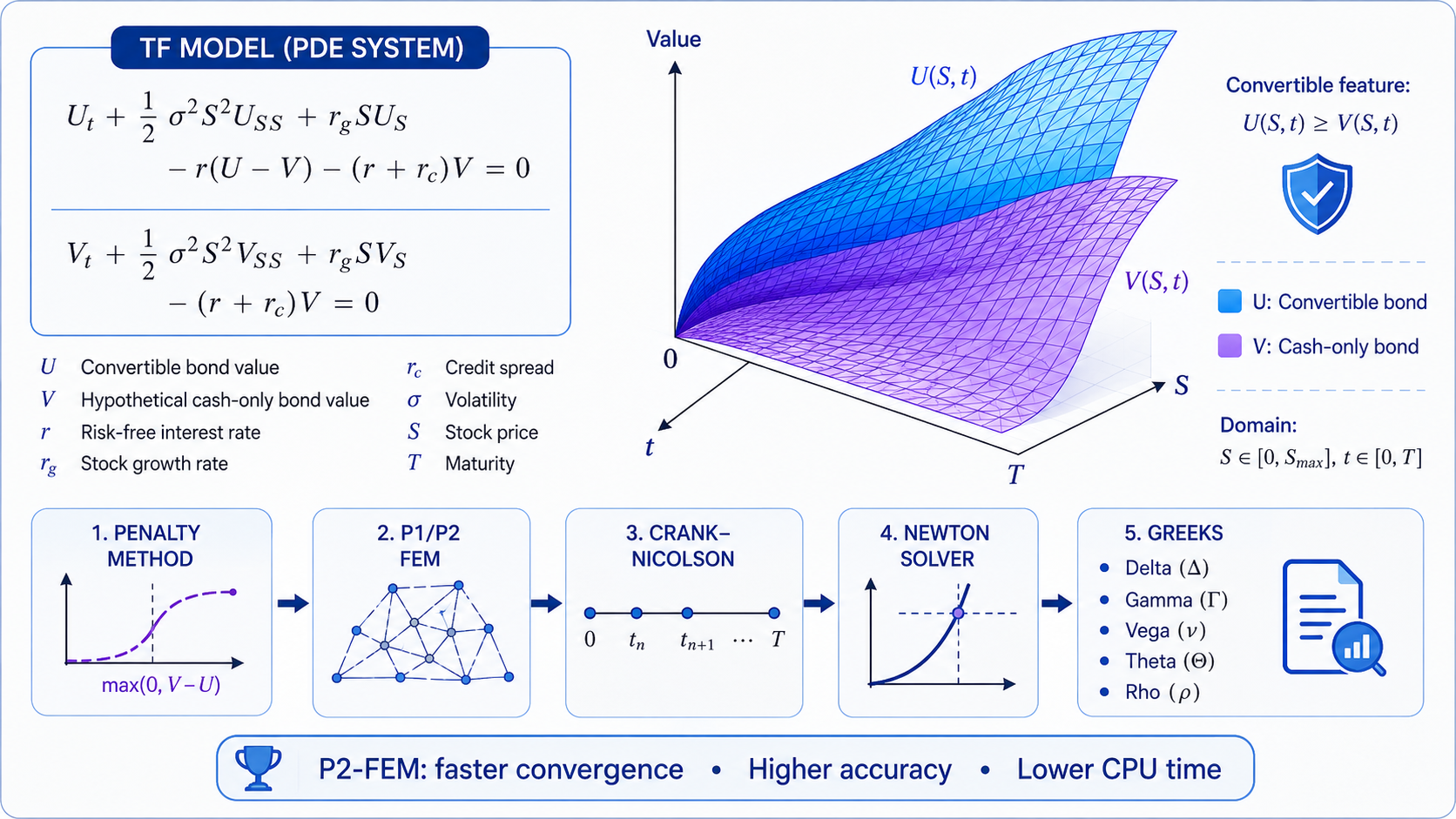

“In this paper, we discuss finite element methods (FEM) for solving numerically the so-called TF model, a PDE-based model for pricing convertible bonds. The model consists of two coupled Black-Scholes equations, whose solutions are constrained. The construction of the FEM is based on the P1 and P2 element, applied to the penalty-based reformulation of the TF model. The resultant nonlinear differential algebraic equations are solved using a modified Crank-Nicolson scheme, with non-linear part with non-smooth terms solved at each time step by Newton’s method. While P1-FEM demonstrates a comparable convergence rate to the standard finite difference method, a better convergence rate is achieved with P2-FEM. The fast convergence of P2-FEM leads to a significant reduction in CPU time, due to the reduction in the number of elements used to achieve the same accuracy as P1-FEM or FDM. As the Greeks are important numerical parameters in the bond pricing, we compute some Greeks using the computed solution and the corresponding FEM approximation functions.”